American Assets Trust (AAT)·Q4 2025 Earnings Summary

American Assets Trust FFO Falls 15% as Office Headwinds Persist, Retail Shines

February 4, 2026 · by Fintool AI Agent

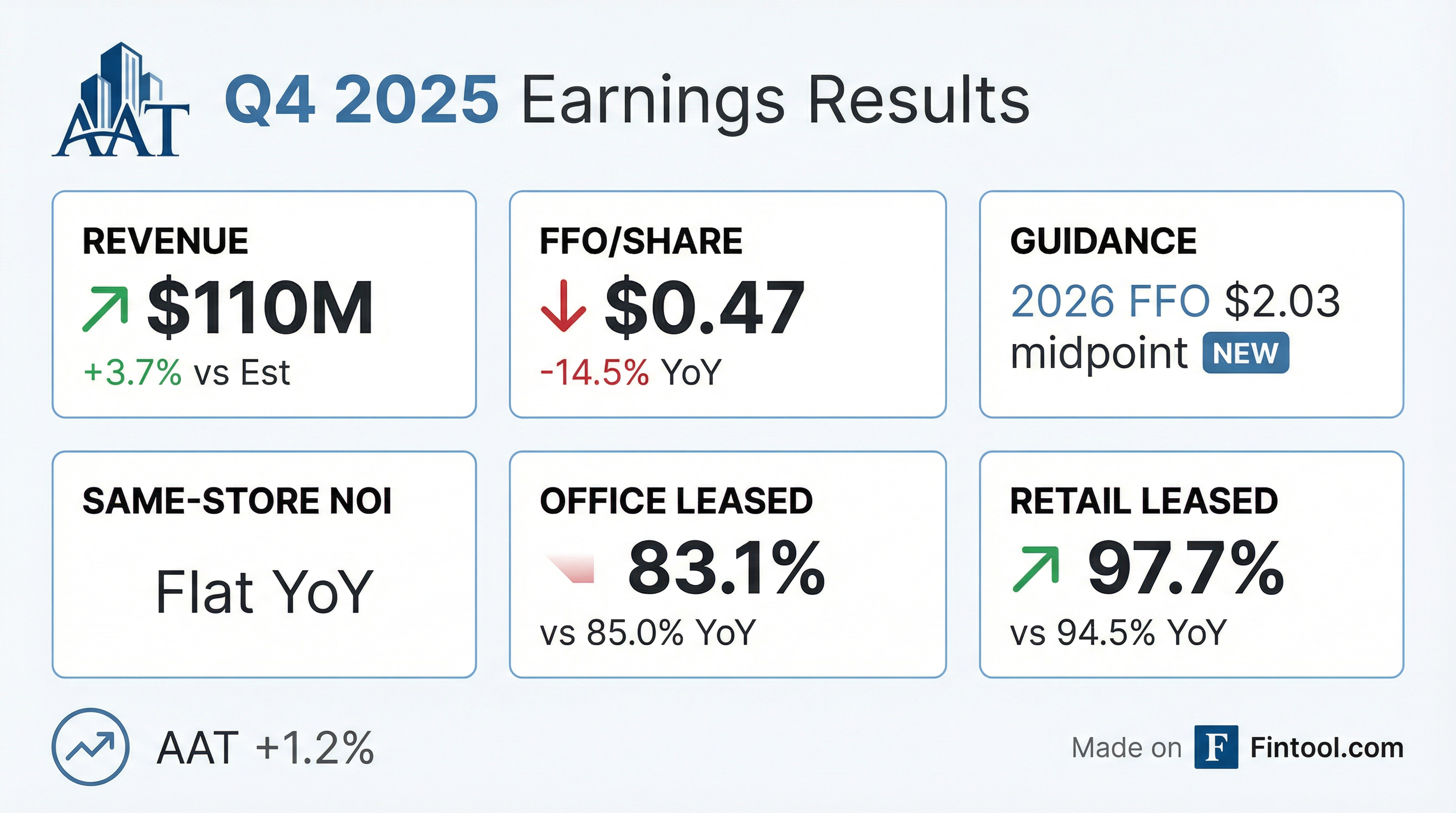

American Assets Trust (NYSE: AAT) delivered a mixed Q4 2025, beating revenue estimates by 3.7% but reporting a 14.5% decline in FFO per share year-over-year . The diversified REIT continues to navigate office market headwinds while benefiting from strength in its retail and multifamily segments. Management introduced 2026 guidance projecting modest FFO growth, signaling stabilization ahead.

Did American Assets Trust Beat Earnings?

Revenue beat, but FFO missed the prior year by a wide margin.

Sources: . Consensus data from S&P Global.

The FFO decline was largely driven by tough year-over-year comparisons. FY 2024 included $11.7M in office lease termination fees and $10.0M in litigation income that didn't repeat in 2025 . Excluding these non-recurring items, FFO per share was $0.47 vs. $0.55 adjusted, still reflecting operational headwinds from lower office occupancy .

What Did Management Guide?

2026 outlook points to stabilization, not acceleration.

AAT introduced full-year 2026 FFO guidance of $1.96-$2.10 per diluted share, with a midpoint of $2.03 . This represents modest 1.5% growth from the $2.00 FFO/share reported in 2025 .

Source:

Key assumptions embedded in guidance:

- No material acquisitions or dispositions beyond announced transactions

- Interest rate environment and credit spreads remain stable

- Current leasing momentum continues

Key drivers of the 2026 outlook from the guidance bridge :

- Same-store NOI growth contributes +$0.10/share (Office +$0.06, Retail +$0.02, Multifamily +$0.01, Mixed-use -$0.01)

- Non-same-store assets (La Jolla Commons 3 + Genesee Park) contribute +$0.03/share

- Lower G&A adds +$0.04/share from reduced professional fees

- Credit reserves deduct -$0.04/share ($0.02 office, $0.02 retail)

- Higher interest expense deducts -$0.02/share from end of capitalized interest at La Jolla Commons 3

- Lower interest income deducts -$0.02/share

- Absence of 2025 termination fees deducts -$0.025/share

What Changed From Last Quarter?

Office pressure continued, but leasing velocity improved significantly.

The sequential story shows stabilization in progress:

Source:

Q4 leasing was the strongest quarter of the year with 236,800 square feet of office and retail space signed, plus 466 multifamily apartment leases . Office leasing spreads came in at +6.6% on a cash basis and +11.5% straight-line, demonstrating pricing power despite occupancy challenges .

How Is the Office Portfolio Performing?

Occupancy down YoY, but rent spreads remain positive.

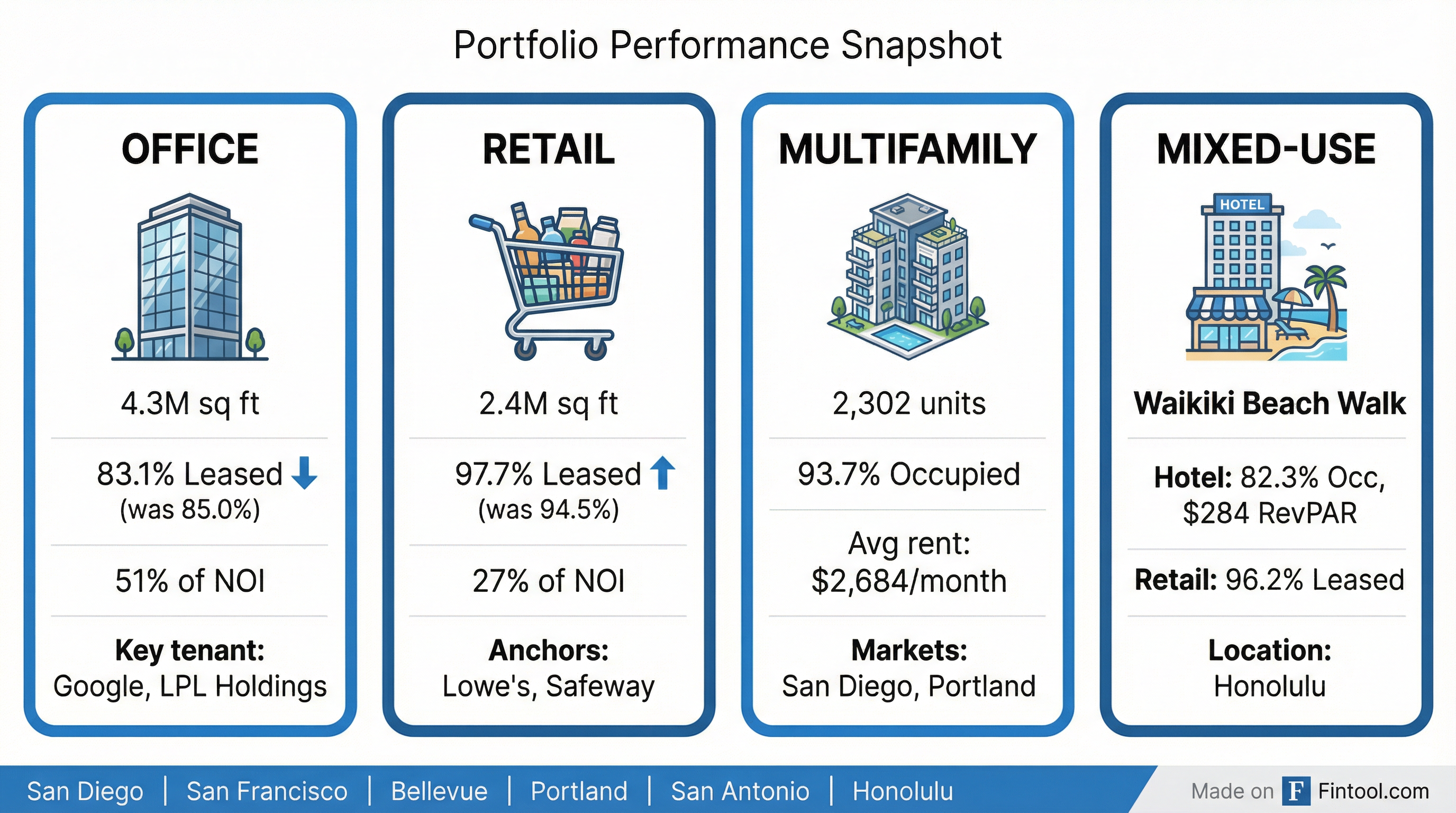

The office segment, representing 51% of NOI, continues to face headwinds from the post-pandemic work-from-home shift :

*Source: *

Despite lower occupancy, same-store office cash NOI actually increased 1.2% in Q4 and 2.5% for the full year, reflecting higher rents on renewed leases and achieved the highest ever average base rents in the office portfolio .

2026 Leasing Momentum is Strong: Management disclosed significant leasing activity heading into 2026 :

- 68,000 sq ft already signed in 11 deals year-to-date

- 214,000 sq ft in active lease documentation

- 235,000 sq ft in proposals management rates at >50% probability

Management is targeting 86%-88% office leased by year-end 2026, representing a 400 bps improvement from 83% at year-end 2025 .

Key tenants include:

- Google at The Landmark at One Market (253K SF, 13.7% of office ABR)

- LPL Holdings at La Jolla Commons (421K SF, 10.5% of office ABR)

- Autodesk at The Landmark (139K SF, 6.8% of office ABR) — extended early with strong renewal rent

How Is the Retail Portfolio Performing?

Retail continues to be the bright spot.

The retail segment delivered impressive leasing spreads and near-full occupancy :

*Source: *

The 24.3% straight-line rent increase on comparable retail leases demonstrates strong pricing power in AAT's high-barrier West Coast and Hawaii markets . Top retail anchors include Lowe's, Safeway, and Sprouts Farmers Market .

How Did the Stock React?

Positive reaction following strong leasing commentary on the call.

AAT shares closed at $18.08 on February 3 (up 1.2% on the earnings release), then rallied +2.9% on February 4 following the earnings call to trade at $18.60. The stock remains:

- 22% below its 52-week high of $23.76

- 11% above its 52-week low of $16.69

- Near its 50-day moving average of $18.73

The post-call rally suggests investors were encouraged by the strong leasing pipeline (68K sq ft already signed in 2026, 214K in documentation), management's confidence in reaching 86%-88% office occupancy by year-end, and the AI tenant activity at One Beach Street.

How Are Development Properties Leasing Up?

La Jolla Commons III and One Beach Street are gaining traction.

Management provided detailed updates on their key development/redevelopment assets :

La Jolla Commons III is attracting "really high-quality tenants" including a legal SaaS company, a prominent insurance company, and the wealth management arm of an international bank . Management expects spec suite revenue to commence this year.

One Beach Street saw a breakthrough with 21% of additional space leased after Q4. The first tenant (commencing rent April 2) is an AI company, with proposals out on 46% of the building . Spec suite permitting is complete with work underway .

CFO Bob Barton reiterated the $0.30/share FFO contribution expected from these assets once stabilized — "It's just a question of timing."

What's the Balance Sheet Position?

Conservative leverage with ample liquidity.

AAT maintains an investment-grade balance sheet with significant financial flexibility :

*Source: *

Credit ratings remain stable at BBB (Fitch), Baa3 (Moody's), and BBB- (S&P) . Only 1 of 31 properties is encumbered by a mortgage .

The company extended its $400M revolving credit facility to early July 2026 and expects to close on the recast in Q2 2026 . CFO Bob Barton noted the banking syndicate is supportive of either $400M or $500M capacity, with the company leaning toward $500M .

On leverage reduction, Barton stated the 5.5x net debt/EBITDA target depends on leasing up La Jolla Commons III and One Beach Street: "The sooner we can get those properties leased up, we will be at the very low end of 6, and then from there, we'll work down to the 5.5."

What About the Dividend?

Dividend maintained at $0.34/share quarterly.

AAT declared a Q1 2026 dividend of $0.340 per share, unchanged from Q4 2025 . The annualized dividend of $1.36 represents:

- 7.5% dividend yield at current prices

- 68% FFO payout ratio based on 2025 FFO

- 67% payout ratio based on 2026 guidance midpoint

CFO Bob Barton noted the 2025 payout ratio was just under 100% due to elevated CapEx spending, but the 2026 outlook implies ~89% payout ratio. Management expects this to trend toward their 85% target beyond 2026 as development assets stabilize . The dividend of $0.34/share is payable March 19 to stockholders of record on March 5 .

What Did Analysts Ask?

Key Q&A highlights from the earnings call:

On elevated tenant improvements: When asked about high Q4 TI spending, EVP Steve Center clarified that two early renewals — Autodesk and Smartsheet — skewed the numbers: "When you strip those two renewals out of the metric on the TIs, the remainder is at $6.41 versus $31." Both tenants extended early because their current space is "critical" to operations.

On path back to 90%+ occupancy: Management sees a two-year timeline as "within the realm of reason" but won't overpromise: "We're really poised to do it now. We've made the investment in the spec suites... we've got really a lot of great inventory that's not gonna take a bunch of time to deliver."

On leasing activity surprises: Steve Center noted multiple unexpected wins: "We've had tenants come out of nowhere that turn into leases... touring a spec suite one week, and then we're in leases the next." Examples include quick conversions at Torrey Reserve and City Center Bellevue where tenants rejected acquisition offers and signed new leases instead .

On AI-driven demand: The first tenant at One Beach Street is an AI company, with "several other tenants we're seeing in Bellevue are AI as well."

On asset sales and share price frustration: CEO Adam Wyll expressed significant frustration with AAT's valuation, noting the stock "fails to reflect the trophy nature of our primarily coastal portfolio." On asset sales: "We're not gonna sell assets at a discount just to check a box... we feel like we have time on our side to be selective."

On guidance upside: CFO Bob Barton identified three factors that could push results toward the high end of guidance: (1) converting speculative office leasing earlier in the year, (2) collecting rents from reserved tenants, and (3) better-than-budgeted multifamily and mixed-use performance .

Key Risks to Monitor

Three areas warrant close attention:

-

Office Lease Expirations: 8.1% of office square footage expires in 2026, including VMware's 18,581 SF expiring January 2026

-

Interest Rate Sensitivity: The credit facility recast in H1 2026 will reprice debt in the current elevated rate environment

-

Waikiki Hotel Volatility: The mixed-use Embassy Suites saw occupancy decline to 82.3% from 85.9% YoY, with RevPAR down 5%

The Bottom Line

American Assets Trust delivered a Q4 that met low expectations, but the earnings call painted a more optimistic picture. The 14.5% FFO decline reflects tough comps and persistent office headwinds, but leasing momentum is accelerating with 68K sq ft already signed in 2026 and 449K sq ft in the active pipeline.

Management is targeting 86%-88% office occupancy by year-end 2026 (up 400 bps), with AI tenants emerging as a demand driver at One Beach Street. The guidance of $2.03 FFO/share at the midpoint signals modest growth, but multiple paths to upside exist if leasing converts earlier than expected.

With a 7.3% dividend yield (based on current price), investment-grade balance sheet, and $0.30/share of FFO upside from development stabilization, AAT offers income investors an asymmetric play on West Coast office recovery — with retail and multifamily providing cash flow stability while office turns the corner.

Related Links: